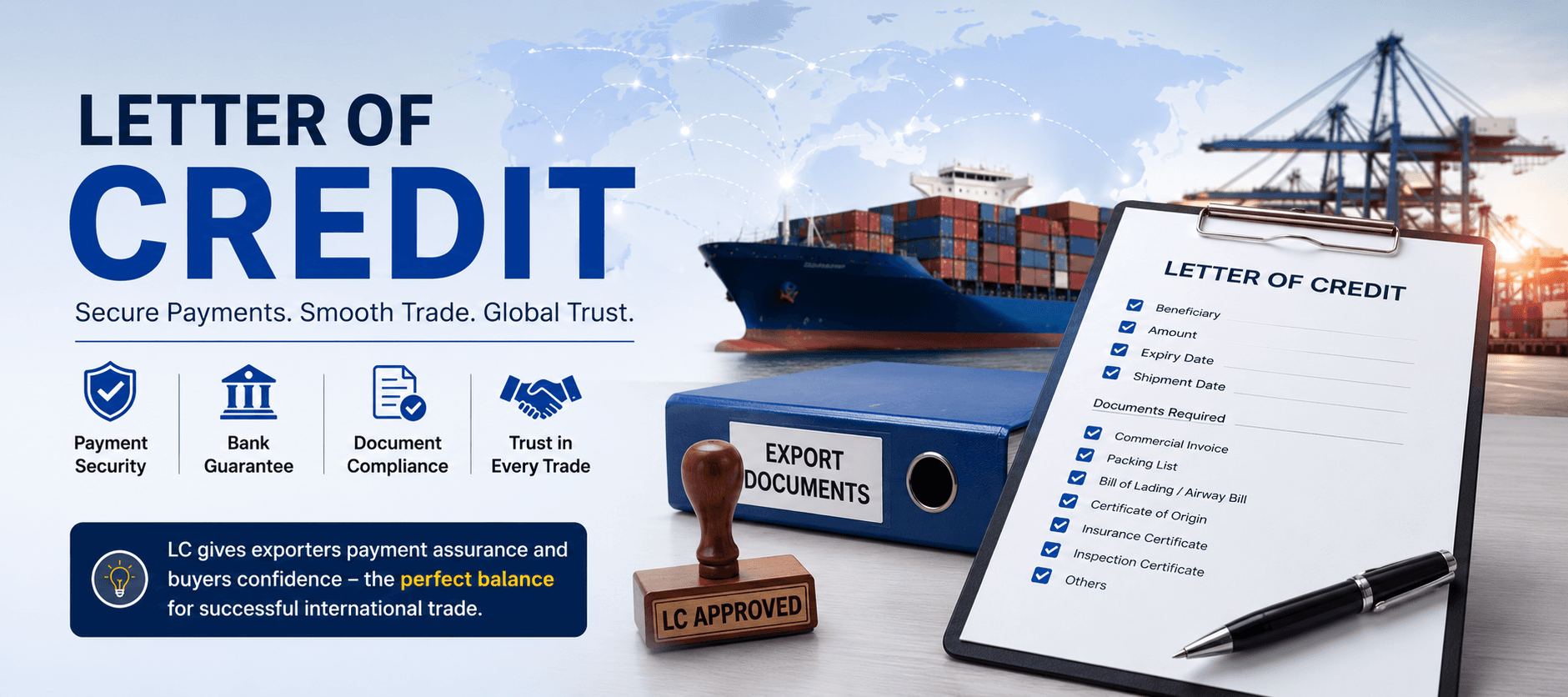

What is a Letter of Credit and How Does It Work?

New to export business? Learn what a Letter of Credit (LC) is, how it works step by step, the parties involved, types of LC, and how to use it safely to guarantee payment in international trade.

What is a Letter of Credit and How Does It Work?

If you are new to export business, one term you will hear constantly is Letter of Credit — or simply LC. Banks mention it. Experienced exporters swear by it. Training programs teach it as a core topic.But for most beginners, the concept feels complicated and confusing.

This guide breaks it down completely — in simple language, with a step-by-step explanation of how it works, why it matters, and what you need to know before using one.

What is a Letter of Credit?

A Letter of Credit is an official document issued by a bank on behalf of a buyer, guaranteeing that the exporter (seller) will receive payment — provided they submit the correct shipping and trade documents within the agreed timeframe.In simple terms: the buyer's bank makes a written promise to pay the exporter.

This is why Letter of Credit is considered one of the most secure payment methods in international trade. The payment guarantee does not depend on the buyer's goodwill or financial situation — it depends on the bank.

Why is Letter of Credit Important in Export Business?

In domestic trade, buyers and sellers often know each other personally. Trust is built over time and legal action is relatively straightforward.In international trade, the situation is completely different. The exporter and buyer may never have met. They are in different countries, different legal systems, and different currencies. If a dispute arises, resolving it is expensive and slow.

This creates two problems:

- The exporter is afraid to ship goods without payment guarantee

- The buyer is afraid to pay before receiving goods

Both parties are protected. This is why LC is widely used for large international orders, new buyer relationships, and high-value export shipments.

Who Are the Parties Involved in a Letter of Credit?

Understanding an LC becomes much easier once you know the key players:1. Applicant (Buyer / Importer)

The buyer who requests their bank to issue the Letter of Credit. They instruct the bank on the terms and conditions of payment.2. Issuing Bank

The buyer's bank that creates and issues the Letter of Credit. This bank takes the responsibility of making payment to the exporter if all conditions are met.3. Beneficiary (Seller / Exporter)

The exporter who receives the Letter of Credit. They will be paid once they submit the required documents correctly and on time.4. Advising Bank

A bank in the exporter's country that receives the LC from the issuing bank and forwards it to the exporter. It verifies the LC's authenticity before passing it on.5. Confirming Bank (Optional)

Sometimes, the exporter asks a bank in their own country to add its own guarantee to the LC. This adds an extra layer of payment security, especially useful when the issuing bank is in a risky country.6. Negotiating Bank

The bank that checks the exporter's documents and processes the payment claim.How Does a Letter of Credit Work? Step by Step

Here is the complete LC process explained in simple steps:Step 1 — Buyer and Seller Agree on Terms

The exporter and buyer negotiate the order. They agree that payment will be made through a Letter of Credit. The sales contract mentions this clearly.Step 2 — Buyer Applies for LC at Their Bank

The buyer goes to their bank (issuing bank) and requests a Letter of Credit in favour of the exporter. The buyer provides details like the exporter's name, order value, required documents, shipment deadline, and expiry date of the LC.Step 3 — Issuing Bank Issues the LC

The buyer's bank verifies the buyer's creditworthiness and issues the Letter of Credit. The LC is then sent to the advising bank in the exporter's country.Step 4 — Advising Bank Forwards LC to Exporter

The advising bank checks the LC's authenticity and forwards it to the exporter. The exporter now has the bank's payment guarantee in hand.Step 5 — Exporter Reviews the LC Carefully

This step is critical. The exporter must read every condition in the LC carefully — product description, quantity, packaging, required documents, shipment date, and expiry date. If anything is incorrect or impossible to comply with, the exporter must request an amendment before starting production.Step 6 — Exporter Ships the Goods

Once the exporter is satisfied with the LC terms, they produce and ship the goods before the deadline mentioned in the LC.Step 7 — Exporter Prepares and Submits Documents

After shipment, the exporter collects all required documents. These typically include the commercial invoice, packing list, bill of lading or airway bill, certificate of origin, inspection certificate, and insurance documents. These are submitted to their bank (negotiating bank) within the LC's validity period.Step 8 — Bank Checks the Documents

The negotiating bank verifies that every document matches the LC conditions exactly. Even minor discrepancies — a spelling error, a wrong date, or a missing stamp — can result in the bank refusing to process payment. This is why document accuracy is so important.Step 9 — Payment is Released

If the documents are in order, the negotiating bank forwards them to the issuing bank. The issuing bank releases payment to the exporter's bank. The exporter receives their money.Step 10 — Buyer Receives Documents and Clears Goods

The issuing bank releases the shipping documents to the buyer. The buyer uses these documents to collect the goods from the port.What Documents Are Typically Required Under an LC?

The exact documents depend on the LC terms, but the most commonly required ones are:- Commercial Invoice — Details of the goods, value, and buyer-seller information

- Packing List — Breakdown of how goods are packed

- Bill of Lading / Airway Bill — Proof that goods were shipped

- Certificate of Origin — Confirms the country where goods were manufactured

- Inspection Certificate — Third-party quality confirmation

- Insurance Certificate — Proof that goods are insured during transit

- Draft / Bill of Exchange — A formal payment demand document

Missing or incorrect documents are the most common reason LC payments are delayed or rejected.

Types of Letter of Credit

There are several types of LC used in international trade, each suited to different situations:Revocable LC

Can be changed or cancelled by the issuing bank without informing the exporter. This type offers very little protection and is rarely used today.Irrevocable LC

Cannot be changed or cancelled without the agreement of all parties. This is the standard type used in most export transactions and offers strong payment security.Confirmed LC

A confirming bank in the exporter's country adds its own payment guarantee on top of the issuing bank's guarantee. Useful when the issuing bank or the buyer's country carries higher risk.Sight LC

Payment is made immediately when the exporter presents compliant documents to the bank. The exporter gets paid on the spot.Usance LC (Deferred Payment LC)

Payment is made after a fixed period — for example, 30, 60, or 90 days after the document presentation date. This gives the buyer time to sell the goods before paying.Revolving LC

Automatically reinstates after each use, up to a fixed limit. Useful when there are regular repeat shipments between the same buyer and seller.Transferable LC

Allows the exporter (beneficiary) to transfer part or all of the credit to another party — often a supplier or manufacturer. Useful for trading companies.Standby LC

Works as a backup guarantee. Payment is only triggered if the buyer fails to fulfil their payment obligation by other means. Similar in concept to a bank guarantee.Advantages of Letter of Credit for Exporters

- Payment is guaranteed by the bank, not just the buyer

- Reduces the risk of buyer default significantly

- Creates a legally structured payment framework

- Suitable for new buyers where trust has not yet been established

- Protects against political risks in the buyer's country (especially with a confirmed LC)

- Gives banks confidence to offer pre-shipment finance against the LC

Risks and Challenges in Letter of Credit

An LC is powerful — but it is not risk-free if you do not handle it carefully.Document discrepancies are the biggest challenge. If your documents do not match the LC terms precisely, the bank can refuse payment. Even small errors — a wrong unit of measurement, a slightly different product description — can cause rejection.

Fraudulent LCs are a real threat. Some dishonest buyers send fake or unverifiable LCs to pressure exporters into shipping goods. Always verify an LC through your own bank before doing anything.

Tight deadlines in LCs can be difficult to meet, especially for manufactured goods. If you miss the shipment date or document submission deadline, the LC expires and payment is no longer guaranteed.

High bank charges — both the issuing bank and advising/confirming banks charge fees. These costs need to be factored into your pricing.

Important Tips for Exporters Using Letter of Credit

- Verify the LC before starting production. Never begin manufacturing based on a verbal LC promise. Wait until the LC reaches your advising bank and has been authenticated.

- Read every condition carefully. Check product description, quantity, packaging requirements, required documents, shipment date, and LC expiry date. If anything cannot be met, request an amendment immediately.

- Prepare documents with zero errors. One wrong spelling or mismatched figure can delay your entire payment. Use a checklist and have your bank or a professional review documents before submission.

- Work with an experienced bank or freight forwarder. For beginners especially, having a knowledgeable partner to guide document preparation is invaluable.

- Prefer irrevocable and confirmed LCs. These offer the strongest protection. Be cautious about usance or revocable terms, especially with new buyers.

Letter of Credit vs Other Payment Methods

| Payment Method | Safety for Exporter | Safety for Buyer | Best For ||---|---|---|---|

| Advance Payment | Highest | Lowest | New buyers, small orders |

| Letter of Credit | High | High | Large orders, new relationships |

| Documents Against Payment | Medium | Medium | Established relationships |

| Open Credit | Lowest | Highest | Trusted, long-term buyers only |

For most exporters dealing with new international buyers on significant order values, Letter of Credit remains the gold standard of payment security.

Frequently Asked Questions

1. Is a Letter of Credit safe for exporters?

Yes — a properly verified, irrevocable Letter of Credit issued by a reputable bank is one of the safest payment methods in international trade. Payment depends on the bank, not the buyer.2. What happens if documents have discrepancies?

The bank will issue a notice of discrepancy. The exporter can either correct the documents (if time permits), seek a waiver from the buyer, or in some cases, accept payment on a collection basis — though this removes the bank's guarantee.3. Can an LC be cancelled?

An irrevocable LC cannot be cancelled or amended without the agreement of all parties including the exporter. A revocable LC can be changed by the issuing bank, which is why irrevocable LCs are strongly preferred.4. How long does an LC take to process?

After all documents are submitted correctly, payment under a sight LC typically takes 5 to 10 working days. Usance LCs pay after the agreed deferred period.5. What is the difference between LC and bank guarantee?

A Letter of Credit is a primary payment instrument — the bank pays when documents are presented. A bank guarantee is a secondary instrument — the bank pays only if the applicant defaults. An LC is used in trade transactions; bank guarantees are more common in service contracts and tenders.Conclusion

A Letter of Credit is one of the most important tools in international trade. For exporters, it provides a bank-backed payment guarantee that removes dependence on buyer trust alone. For buyers, it ensures payment is only released when goods are shipped and documented correctly.Understanding how an LC works — the parties involved, the step-by-step process, the types, and the document requirements — is fundamental knowledge for anyone entering export business.

The key to using an LC successfully is simple: verify it before you ship, read every condition carefully, and submit perfect documents on time.

Call To Action

Want to learn how to handle Letters of Credit, export documentation, buyer verification, and payment methods in real business situations?👉 Join GIFT Export Import Course in Ahmedabad

A 100% practical training program built for students, beginners, and entrepreneurs who want to build a safe and successful export career.

🚀 Join GIFT Export Import Training today.

Tags

Frequently Asked Questions

Is a Letter of Credit safe for exporters?

Yes — a properly verified, irrevocable Letter of Credit issued by a reputable bank is one of the safest payment methods in international trade. Payment depends on the bank, not the buyer.

What happens if documents have discrepancies in an LC?

An irrevocable LC cannot be cancelled or amended without the agreement of all parties. A revocable LC can be changed by the issuing bank — which is why irrevocable LCs are strongly preferred.

How long does a Letter of Credit take to process?

After all documents are submitted correctly, payment under a sight LC typically takes 5 to 10 working days. Usance LCs pay after the agreed deferred period.

What is the difference between a Letter of Credit and a bank guarantee?

A Letter of Credit is a primary payment instrument — the bank pays when documents are presented. A bank guarantee is secondary — the bank pays only if the applicant defaults. LC is used in trade; bank guarantees are common in service contracts and tenders.